Bluerock Residential Growth REIT Issues Corporate Update and Reports First Quarter 2014 Results

New York, NY – Bluerock Residential Growth REIT, Inc. (NYSE MKT: BRG) (“the Company”), a real estate investment trust (REIT) formed to acquire a diversified portfolio of institutional-quality apartment properties in demographically attractive growth markets throughout the United States, issued financial results for the first quarter ended March 31, 2014, and provides a corporate update to highlight the Company’s progress.

The Company completed a public offering of 3,448,276 shares of Class A common stock at a public offering price of $14.50 per share for total gross proceeds of $50.0 million on April 2, 2014 (the “IPO”) and listing of the Class A common stock on the NYSE MKT exchange for trading. The net proceeds of the offering are estimated to be approximately $44.4 million after deducting underwriting discounts and commissions and estimated offering expenses.

Highlights

- Closing on Acquisitions of Five Properties

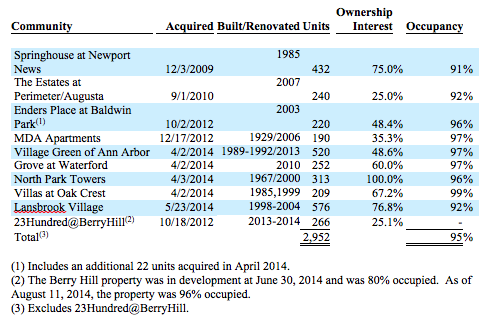

Since completing the IPO, the Company closed on all five of its previously identified contribution transactions. The Company now owns an interest in a portfolio of nine apartment properties comprising an aggregate of 2,620 units. These properties were 94% occupied of March 31, 2014, exclusive of the Berry Hill development project. - Berry Hill Development Project Exceeding Projections

The Company’s development project, 23 Hundred at Berry Hill in Nashville, Tennessee, is now 74% pre-leased and the Company expects that the project will be stabilized during the third quarter of 2014. The property is currently achieving rents of $1.88 per square foot, exceeding underwriting assumptions of $1.65 per square foot based. The project is on track to achieve a stabilized return on cost of 8.45% based on latest rents being achieved at the property vs. market cap rates of 5.5% for comparable product as estimated by the Company. - Planned Acquisition of attractive Fractured Condo Project

The Company announced the planned acquisition of a majority joint venture interest in Lansbrook Village, a Class A fractured condominium community located in Tampa, Florida, with an equity investment of approximately $14.2 million. Based on April collections, the property is achieving a yield to cost of 6.65% vs. a market cap rate for the asset of 5.75% as estimated by the company. At the completion of its business plan, including the purchase of additional units, the Company expects the property to attain a 7.40% return on cost. - Gary Kachadurian Joins Board of Directors, to Lead Investment Committee

Gary Kachadurian has joined the Company’s Board of Directors and will chair its investment committee. Mr. Kachadurian is a 30-year industry veteran, and has previously served as head of RREEF’s National Acquisitions Group and Value-Added and Development lines of business, where he had oversight in the acquisition and management of RREEF’s 24,000-unit apartment investment portfolio. Prior to RREEF, Mr. Kachadurian was the Midwest Regional Operating Partner for Lincoln Property Company, developing and managing over 3,000 apartment units. - Monthly Dividends Declared for Second Quarter 2014, at a 9.2% annualized yield

The Company declared monthly cash dividends for the second quarter of 2014 equal to a quarterly rate of $0.29 per share on the Company’s Class A common stock and $0.29 per share of Class B common stock. This equates to a 9.2% annualized yield based on the closing price of $12.61 for the Class A common stock as of May 13, 2014, which is subject to change. - Disposition of Creekside Asset at a 23% IRR, and a 2.0 times equity multiple

The Company successfully completed the sale of The Reserve at Creekside Village, a 192 unit community in Chattanooga, Tennessee on March 28, 2014. The asset, which had been designated “Held for Sale” in the Company’s 2013 year-end financial statements, generated a property level internal rate of return (IRR) of 23% and posted an equity multiple of 2.0x. This is the fourth asset sale by the Company since its inception. Average IRR and equity multiple across those sales, inclusive of the Creekside property, is 43% and 2.2x, respectively. - Engagement of New REIT Manager

The Company entered into a Management Agreement with BRG Manager, an affiliate of Bluerock Real Estate, pursuant to which BRG Manager has primary responsibility for managing the Company’s day-to-day business affairs and its portfolio of real estate investments. The new Management Agreement with BRG Manager is expected to provide an overall lower fee structure than the previous advisory agreement with the Company’s pre-IPO advisor, reducing corporate general and administrative expenses relative to the size of the Company’s portfolio.

Financial Results First Quarter 2014

As noted above, the Company completed a $50 million public offering on April 2, 2014, after the close of the quarter. In light of the IPO, first quarter results are not viewed by management as representative of expected future performance.

Adjusted Funds from Operations, or AFFO, for the first quarter 2014 was $(476,607), or $(0.45) per weighted average diluted common share, as compared to $(360,897), or $(0.36) per weighted average diluted common share, respectively, in the prior year period. The net loss attributable to common stockholders for the first quarter of 2014 was $(1.05) million or a loss of $(0.99) per share compared to a net loss of $(1.23) million or $(1.23) per share in the prior year period. The per share amounts above were calculated based on weighted average shares outstanding of 1,060,889 for the first quarter of 2014 and 995,154 for the prior year period. The primary reason for the Company’s net loss and negative AFFO was the level of general and administrative expenses relative to the size of its portfolio prior to the IPO.

Funds from Operations, or FFO, for the first quarter 2014 was $(959,128), or $(0.90) per weighted average diluted common share, as compared to $(441,935), or $(0.42) per weighted average diluted common share, respectively, in the prior year period. The increase in negative FFO was driven by an increase in asset disposition fees from the sale of our Creekside property. A reconciliation of GAAP net loss to FFO and AFFO for the first quarter 2014 is included below under the heading “Funds from Operations and Adjusted Funds from Operations”.

Total assets decreased $16.1 million to $156.4 million as of March 31, 2014 from $172.5 million as of December 31, 2013, and total liabilities decreased $10.7 million to $115.7million as of March 31, 2014 from $126.4 million as of December 31, 2013. This decrease resulted from the sale of the Creekside property which had a book value of $19.3 million and a $12.5 million mortgage that was paid in full upon sale. This decrease was offset by $3.4 million of construction activity funded by a construction loan at our Berry Hill property.

Management Commentary

“With the completion of the public offering we feel we will be able to grow our asset base more quickly with acquisitions that we believe to be accretive and provide substantial income and NAV growth potential, particularly in light of our current pipeline,” Mr. Kamfar, said.

Within the next 60 days, the Company intends to deploy its remaining capital from the IPO by making additional property investments. “We are seeking to position the Company to provide a dividend fully covered by adjusted funds from operations, when we have fully invested our funds and stabilized the properties,” said Mr. Kamfar.

Dividend Details

On April 8, 2014, the Company’s Board of Directors declared monthly dividends for the second quarter of 2014 equal to a quarterly rate of $0.29 per share on the Company’s Class A common stock and $0.29 per share on the Company’s Class B common stock, payable to stockholders of record as of April 25, 2014, May 25, 2014 and June 25, 2014. Holders of OP and LTIP units are entitled to receive “distribution equivalents” at the same time as dividends are paid to holders of the Company’s Class A common stock.

The declared dividends equal a monthly dividend on the Class A common stock and the Class B common stock as follows: $0.096666 per share for the dividend paid to stockholders of record as of April 25, 2014, $0.096667 per share for the dividend paid to stockholders of record as of May 25, 2014, and June 25, 2014.

Acquisition and Disposition Activity Details

Acquisition of North Park Towers: On April 3, 2014, the Company acquired a 313-unit multifamily property located in Southfield, Michigan in exchange for OP Units with an approximate value of $4.1 million, net of the assumed mortgage indebtedness of approximately $11.5 million.

Acquisition of Interest in Village Green of Ann Arbor: On April 2, 2014, the Company acquired a controlling, indirect equity interest in a 520-unit multifamily property located in Ann Arbor, Michigan in exchange for unregistered shares of Class A common stock with a value of approximately $7.0 million. The property is encumbered by an approximate $43.2 million mortgage loan.

Acquisition of Interest in Villas at Oak Crest: On April 2, 2014, the Company acquired an indirect preferred equity interest in a 209-unit multifamily property located in Chattanooga, Tennessee in exchange for unregistered shares of Class A common stock with a value of approximately $2.9 million. The property is encumbered by an approximate $12.4 million mortgage loan.

Acquisition of Additional Interest in Springhouse at Newport News: On April 2, 2014, the Company acquired additional indirect equity interest in a 432-unit multifamily property located in Newport News, Virginia, for approximately $3.5 million in cash.

Acquisition of Interest in Grove at Waterford: On April 2, 2014, the Company acquired a controlling, indirect equity interest in a 252-unit multifamily property located in Hendersonville, Tennessee, in exchange for unregistered shares of Class A common stock with a value of approximately $5.2 million and $600,000 in cash.

Acquisition of Majority Joint Venture Interest in Lansbrook Village: On May 8, 2014, the Company’s Board approved the acquisition of a majority joint venture interest in 573 units out of a 774-unit condominium community known as Lansbrook Village, a Class A fractured condominium community located in the Tampa, Florida suburb of Palm Harbor.

Disposition of The Reserve at Creekside: On March 28, 2014, an entity in which the Company holds an indirect equity interest, sold the Creekside property to an unaffiliated third party for approximately $18.9 million, which generated net proceeds to the Company of approximately $1.2 million and an IRR of 23%.

Funds from Operations and Adjusted Funds from Operations

Funds from operations, or FFO, is a non-GAAP financial measure that is widely recognized as a measure of REIT operating performance. The Company considers FFO to be an appropriate supplemental measure of its operating performance as it is based on a net income analysis of property portfolio performance that excludes non-cash items such as depreciation. The historical accounting convention used for real estate assets requires straight-line depreciation of buildings and improvements, which implies that the value of real estate assets diminishes predictably over time. Since real estate values historically rise and fall with market conditions, presentations of operating results for a REIT, using historical accounting for depreciation, could be less informative. The Company defines FFO, consistent with the National Association of Real Estate Investment Trusts, or NAREIT’s, definition, as net income, computed in accordance with GAAP, excluding gains (or losses) from sales of property, plus depreciation and amortization of real estate assets, and after adjustments for unconsolidated partnerships and joint ventures. Adjustments for unconsolidated partnerships and joint ventures will be calculated to reflect FFO on the same basis.

In addition to FFO, the Company uses adjusted funds from operations, or AFFO. AFFO is a computation made by analysts and investors to measure a real estate company’s operating performance by removing the effect of items that do not reflect ongoing property operations.

The Company further adjusts FFO by adding back certain items that are not added to net income in NAREIT’s definition of FFO, such as acquisition expenses, equity based compensation expenses, and any other non-recurring or non-cash expenses, which are costs that do not relate to the operating performance of the Company’s properties, and subtracting recurring capital expenditures.

The Company’s calculation of AFFO differs from the methodology used for calculating AFFO by certain other REITs and, accordingly, the Company’s AFFO may not be comparable to AFFO reported by other REITs. The Company’s management utilizes FFO and AFFO as measures of operating performance after adjustment for certain non-cash items, such as depreciation and amortization expenses, and acquisition expenses and pursuit costs that are required by GAAP to be expensed but may not necessarily be indicative of current operating performance and that may not accurately compare the Company’s operating performance between periods. Furthermore, although FFO, AFFO and other supplemental performance measures are defined in various ways throughout the REIT industry, the Company also believes that FFO and AFFO may provide the Company and its stockholders with an additional useful measure to compare the Company’s financial performance to certain other REITs. The Company also uses AFFO for purposes of determining the quarterly incentive fee, if any, payable to the Company’s Manager.

Neither FFO nor AFFO is equivalent to net income or cash generated from operating activities determined in accordance with GAAP. Furthermore, FFO and AFFO do not represent amounts available for management’s discretionary use because of needed capital replacement or expansion, debt service obligations or other commitments or uncertainties. Neither FFO nor AFFO should be considered as an alternative to net income as an indicator of the Company’s operating performance or as an alternative to cash flow from operating activities as a measure of our liquidity.

Table 1 presents the Company’s calculation of FFO and AFFO for the three months ended March 31, 2014 and 2013.

{kind=link}

Operating cash flow, FFO and AFFO may also be used to fund all or a portion of certain capitalizable items that are excluded from FFO and AFFO, such as tenant improvements, building improvements and deferred leasing costs.

Presentation of this information is intended to assist the reader in comparing the sustainability of the operating performance of different REITs, although it should be noted that not all REITs calculate FFO or AFFO the same way, so comparisons with other REITs may not be meaningful. FFO or AFFO should not be considered as an alternative to net income (loss) as calculated in accordance with GAAP, as an indication of the Company’s liquidity, nor is either indicative of funds available to fund the Company’s cash needs, including its ability to make distributions. Both FFO and AFFO should be reviewed in connection with other GAAP measurements.

About Bluerock Residential Growth REIT, Inc.

Bluerock Residential Growth REIT, Inc. (NYSE MKT: BRG) is a real estate investment trust formed to acquire a diversified portfolio of institutional-quality apartment properties in demographically attractive growth markets throughout the United States. The Company has elected to be taxed as a real estate investment trust (REIT) for U.S. federal income tax purposes.

Forward Looking Statements

This press release contains forward looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 and other federal securities laws. These forward looking statements are based on the Company’s present expectations, but these statements are not guaranteed to occur, including the 23 Hundred at Berry Hill rents per square foot and market capitalization rates, the Company’s investment in the joint venture that owns the Lansbrook Village property, claims relative to the Company’s pipeline, the Company’s dividends, the fee structure under the Management Agreement, the Company’s future performance, management’s commentary relating to future income and portfolio growth and operating results, dividend coverage and future acquisitions. Furthermore, the Company disclaims any obligation to publicly update or revise any forward-looking statement to reflect changes in underlying assumptions or factors, of new information, data or methods, future events or other changes. Investors should not place undue reliance upon forward looking statements. For further discussion of the factors that could affect outcomes, please refer to the “Risk Factors” section of the prospectus dated March 28, 2014 and filed by the Company with the Securities and Exchange Commission (“SEC”) on April 1, 2014, and subsequent filings by the Company with the SEC.

[box style=”1″] Download PDF[/box]