Bluerock Residential Growth REIT Announces Fourth Quarter 2018 Results

Total Revenues Grew 37% YoY to $50.0 Million

Same Store Revenue Growth of 5.5% YoY

New York, NY (February 14, 2019) – Bluerock Residential Growth REIT, Inc. (NYSE American: BRG) (“the Company”), an owner of highly amenitized multifamily apartment communities, announced today its financial results for the quarter ended December 31, 2018.

Fourth Quarter Highlights

- Total revenues grew 37% to $50.0 million for the quarter from $36.6 million in the prior year period.

- Net loss attributable to common stockholders for the fourth quarter of 2018 was ($0.55) per share, as compared to ($1.87) per share in the prior year period.

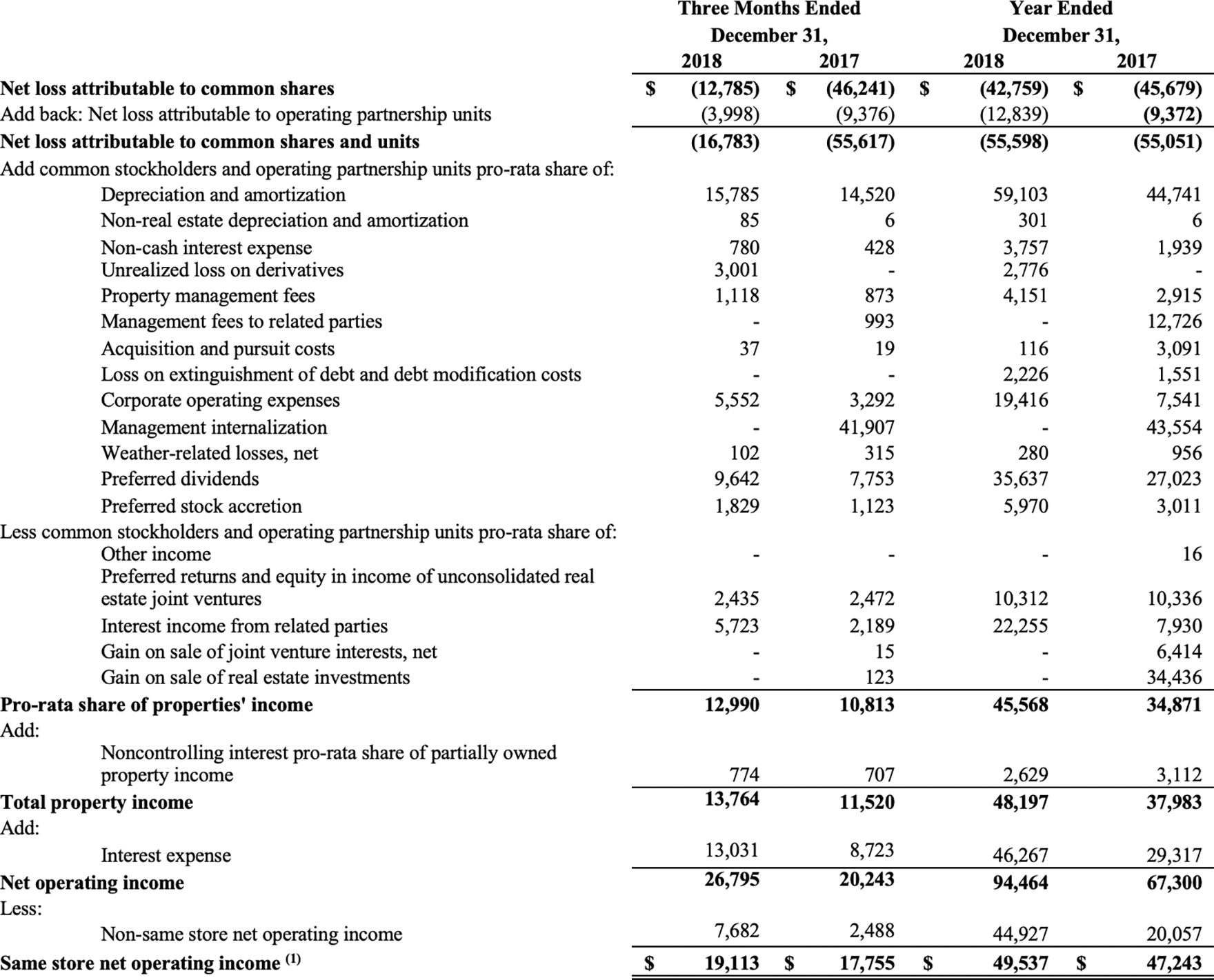

- Property Net Operating Income (“NOI”) grew 32% to $26.8 million, from $20.2 million in the prior year period.

- Same store revenue and NOI increased 5.5% and 7.6% respectively, as compared to the prior year period.

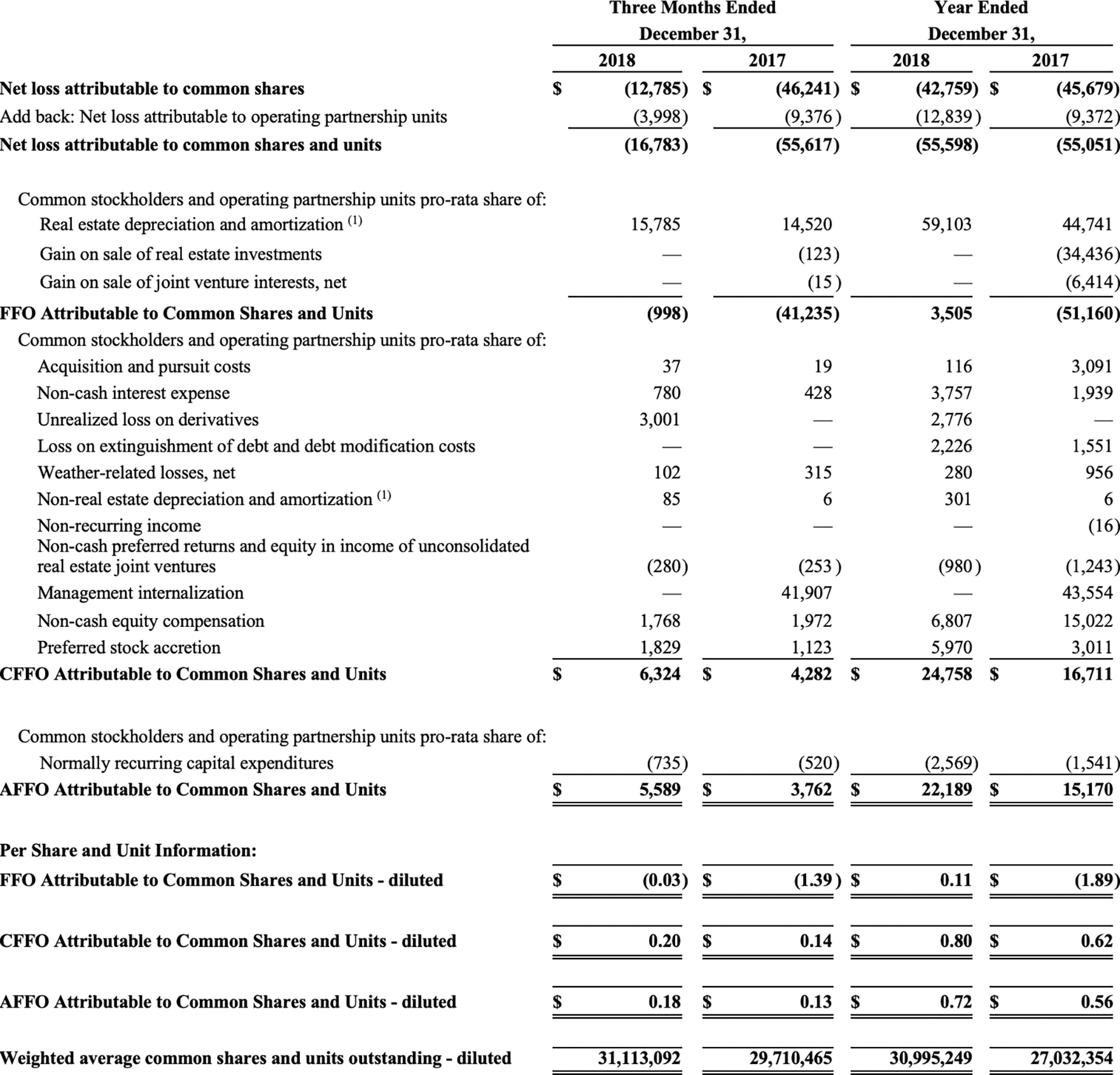

- Core funds from operations attributable to common shares and units (“CFFO”) increased 47% to $6.3 million, from $4.3 million in the prior year period. CFFO per share is $0.20 for the fourth quarter as compared to $0.14 in the prior year period. Dividend payout on a CFFO basis improved to 81% during the fourth quarter.

- Adjusted funds from operations attributable to common shares and units (“AFFO”) grew 48% to $5.6 million, from $3.8 million in the prior year period. AFFO per share is $0.18 for the quarter as compared to $0.13 in fourth quarter 2017.

- Consolidated real estate investments, at cost, increased approximately $349.9 million to $1.8 billion, from December 31, 2017.

- The Company invested approximately $39.7 million for an 85% interest in a multifamily community totaling 512 units with a total purchase price of $143.4 million.

- The Company completed 339 value-add unit upgrades during the quarter.

Full Year 2018 Highlights

- Total revenues grew 49% to $184.7 million for the year from $123.6 million in the prior year.

- Net loss attributable to common stockholders for 2018 was ($1.82) per share, as compared to ($1.79) per share in the prior year.

- Property NOI grew 40% to $94.5 million, from $67.3 million in the prior year.

- Same store revenue and NOI increased 4.5% and 4.9% respectively, as compared to the prior year.

- CFFO increased 49% to $24.8 million, from $16.7 million in the prior year. CFFO per share increased 29% to $0.80 for the year from $0.62 in the prior year.

- AFFO grew 46% to $22.2 million, from $15.2 million in the prior year. AFFO per share grew 29% to $0.72 from $0.56 in the prior year.

- For the full year, the Company made investments in eight properties with 2,309 total units for a total purchase price of $366.5 million.

- The Company completed 1,186 value-add unit upgrades during the year.

“We are pleased to announce another strong quarter of operating results. Property NOI is up over 32% and same store NOI is up 7.6% over the prior year. These results demonstrate the ongoing successful execution of our strategic initiatives. We continue to realize attractive returns on our value-add unit renovation investments along with accretively growing our portfolio with well-located, high quality properties,” said Ramin Kamfar, Company Chairman and CEO. “We again covered our dividend and are pleased with our industry-leading performance. With a robust pipeline of opportunities, we remain committed to our investment strategy and are optimistic about our outlook.”

Financial Results

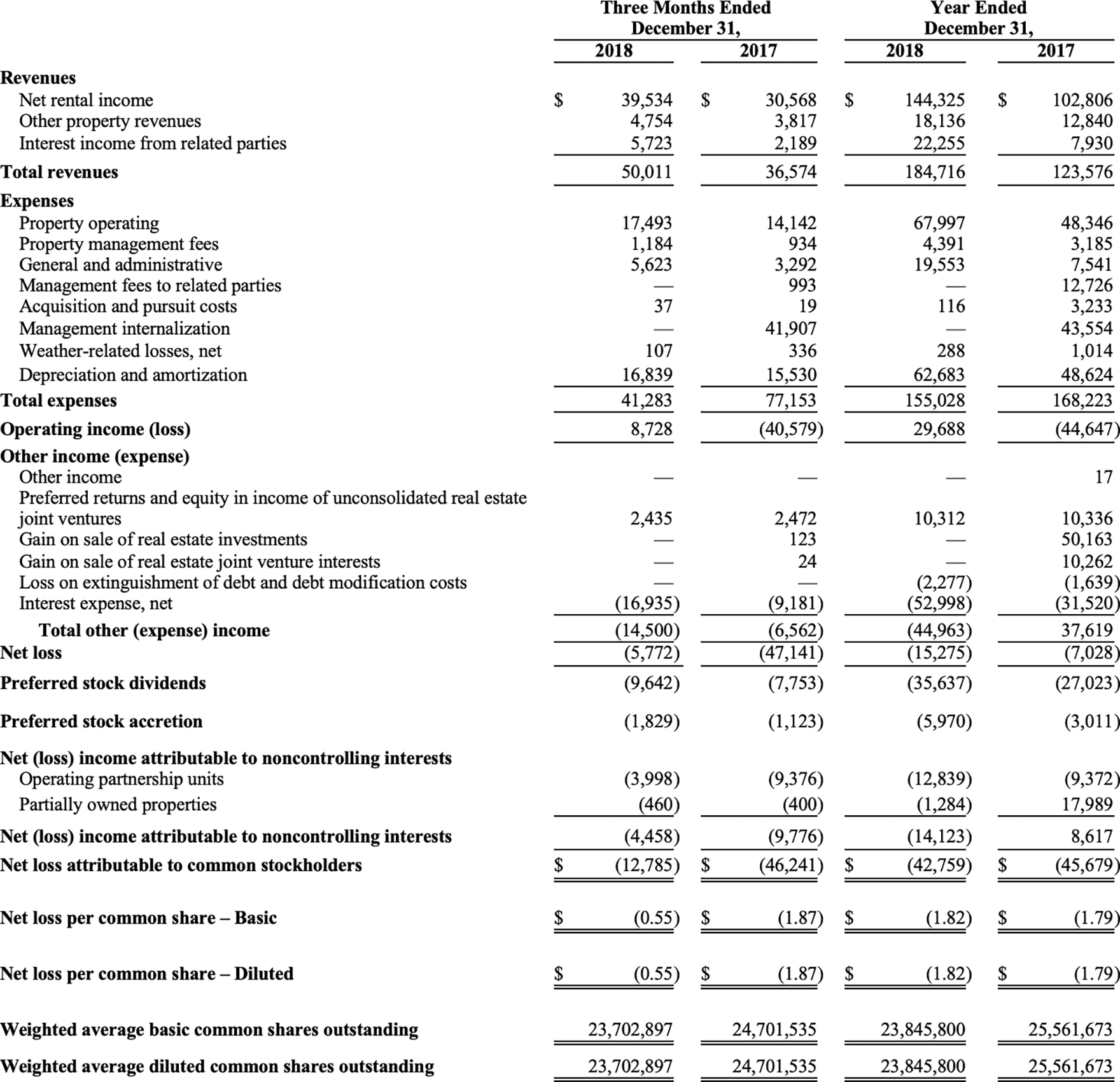

Net loss attributable to common stockholders for the fourth quarter of 2018 was $12.8 million, compared to $46.2 million in the prior year period. Net loss attributable to common stockholders included non-cash expenses of $17.7 million or $0.75 per share in the fourth quarter of 2018 compared to $49.8 million or $2.02 per share for the prior year period.

CFFO for the fourth quarter of 2018 was $6.3 million, or $0.20 per diluted share, compared to $4.3 million, or $0.14 per diluted share in the prior year period. CFFO adds back non-cash, non-operating expenses such as accretion on the Company’s Series B preferred stock. CFFO was primarily driven by growth in property NOI of $6.6 million and interest income of $3.5 million arising from significant investment activity. This was primarily offset by a year-over-year increase in interest expense of $4.4 million, general and administrative expenses of $1.5 million, and preferred stock dividends of $1.9 million.

AFFO for the fourth quarter of 2018 was $5.6 million, or $0.18 per diluted share, compared to $3.8 million, or $0.13 per diluted share in the prior year period.

Total Portfolio Performance

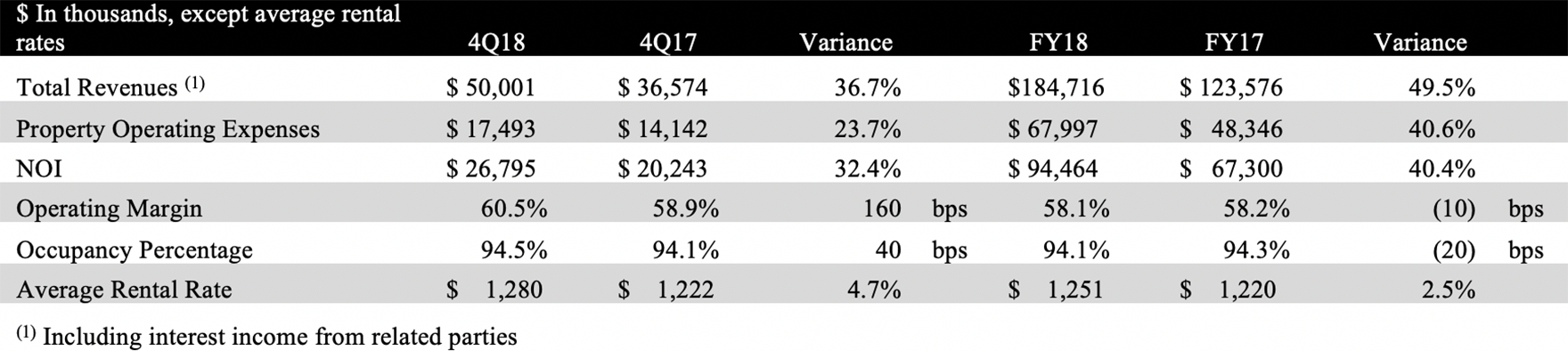

For the fourth quarter of 2018, property revenues increased by 36.7% compared to the same prior year period primarily attributable to the increased size of the portfolio. Total portfolio NOI was $26.8 million, an increase of $6.6 million, or 32.4%, compared to the same period in the prior year. Property operating expenses were up primarily due to the increased size of the portfolio.

Property NOI margins expanded by 160 basis points to 60.5% of revenue for the quarter, compared to 58.9% of revenue in the prior year quarter.

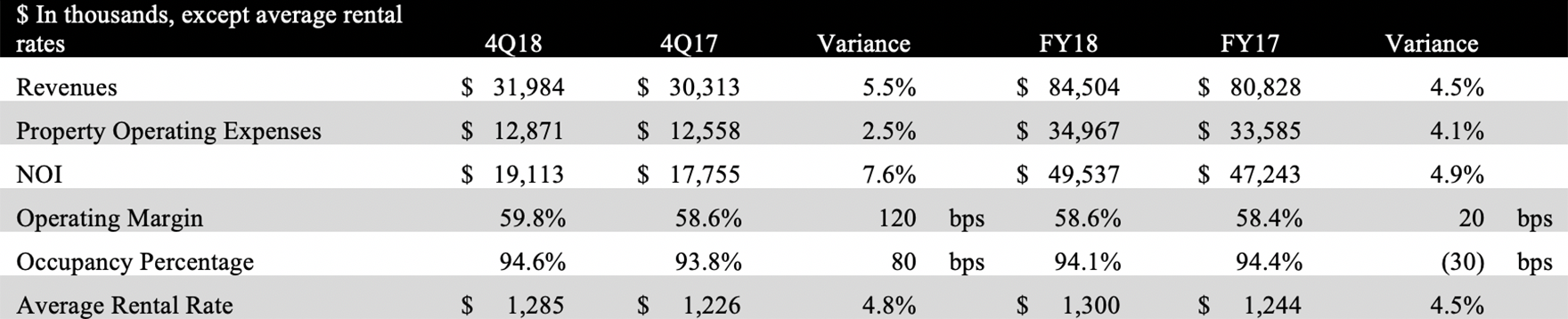

Same Store Portfolio Performance

The Company’s same store portfolio for the quarter ended December 31, 2018 included 24 properties. For the fourth quarter of 2018, same store NOI was $19.1 million, an increase of $1.3 million, or 7.6%, compared to the same period in the prior year. Same store property revenues increased by 5.5% compared to the same prior year period, primarily attributable to a 4.8% increase in average rental rates, as well as average occupancy increasing 80 basis points to 94.6%. Same store expenses increased $0.3 million, primarily due to $0.15 million related to payroll, $0.11 million in maintenance, and $0.09 million of increased real estate taxes.

Renovation Activity

The Company completed 1,186 value-add unit upgrades during the year, including 339 units during the fourth quarter.

Since inception within the existing portfolio, the Company has completed 1,666 value-add unit upgrades at an average cost of $4,824 per unit and achieved an average monthly rental rate increase of $104 per unit, equating to a 25.9% ROI on all unit upgrades leased as of December 31, 2018. The Company has identified approximately 4,800 remaining units within the existing portfolio for value-add upgrades with similar projected economics to the completed renovations. The Company expects to complete between 900 and 1,200 unit renovations in 2019.

Acquisition Activity

On November 15, 2018, the Company acquired an 85% interest in a 512-unit apartment community located in Lakewood, Colorado, known as Ashford Belmar. The total purchase price was approximately $143.4 million, funded in part by a $100.7 million mortgage loan secured by the Ashford Belmar property.

The Company also entered into three development joint ventures with unrelated third parties in the fourth quarter. The development joint ventures are for apartment communities with a total of 631 units in Leander, Texas, Austin, Texas, and Concord, North Carolina. The Company contributed approximately $9.5 million out of total preferred commitments of $40.0 million.

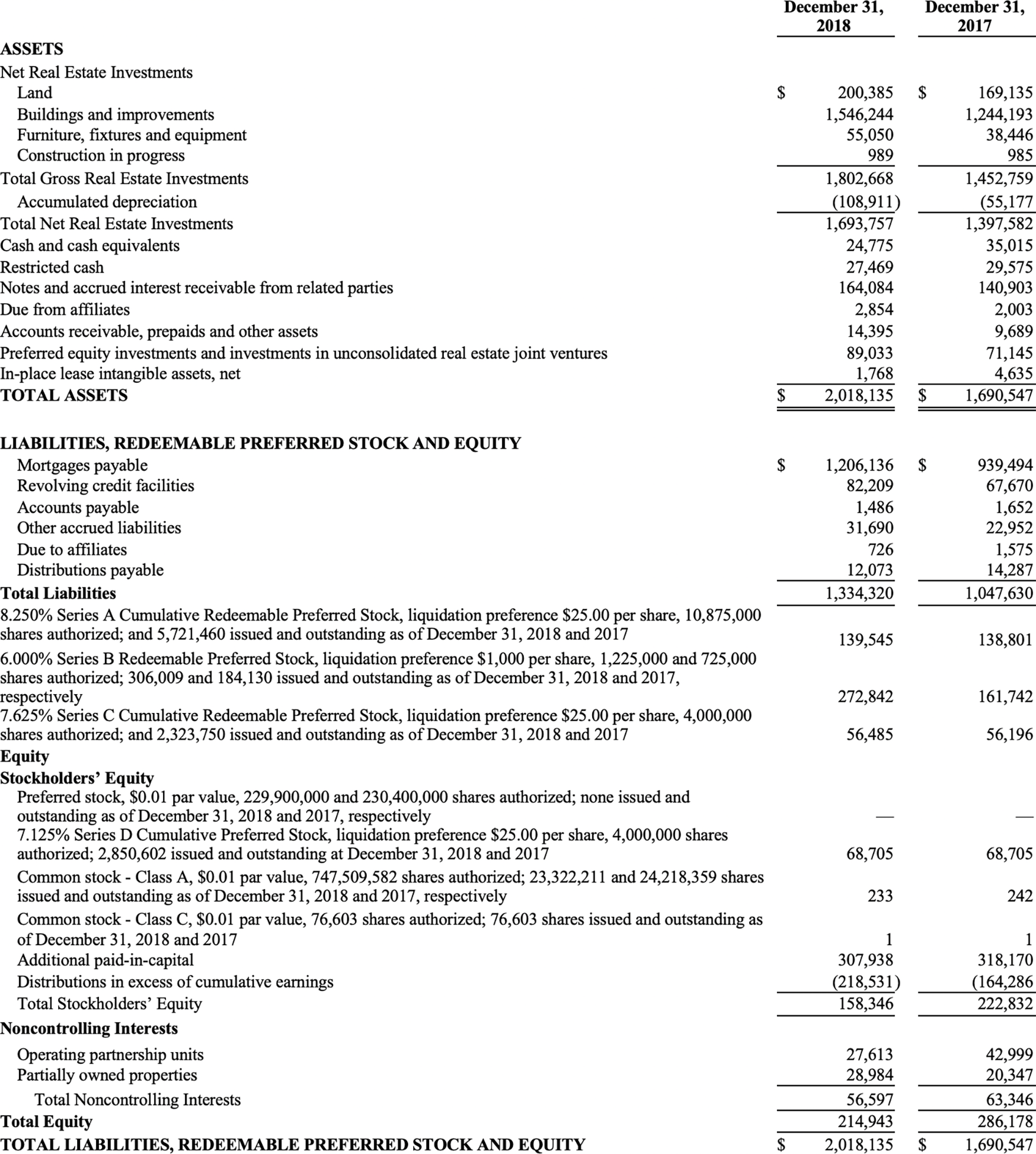

Balance Sheet

During the fourth quarter, the Company raised gross proceeds of approximately $43.7 million through the issuance of 43,656 shares of Series B preferred stock with associated warrants at $1,000 per unit. For the full year 2018, the Company raised gross proceeds of approximately $123.6 million through the issuance of 123,592 shares of Series B preferred stock.

As of December 31, 2018, the Company had $24.8 million of unrestricted cash on its balance sheet, approximately $48.3 million available among its revolving and term credit facilities, and $1.3 billion of debt outstanding.

Dividend

The Board of Directors authorized, and the Company declared, a quarterly dividend for the fourth quarter of 2018 equal to a quarterly rate of $0.1625 per share on its Class A common stock, payable to the stockholders of record as of December 24, 2018, which was paid in cash on January 4, 2019. A portion of each dividend may constitute a return of capital for tax purposes.

On October 12, 2018, the Board of Directors authorized, and the Company declared, a monthly dividend of $5.00 per share of Series B preferred stock, payable to the stockholders of record as of October 25, 2018, November 23, 2018, and December 24, 2018 which were paid in cash on November 5, 2018, December 5, 2018, and January 4, 2019, respectively.

2019 Guidance

Based on the Company’s current outlook and market conditions, the Company anticipates 2019 CFFO in the range of $0.80 to $0.84 per share. For additional guidance details underlying earnings guidance, please see page 31 of Company’s Fourth Quarter 2018 Earnings Supplement available under Investor Relations on the Company’s website (www.bluerockresidential.com).

Conference Call

All interested parties can listen to the live conference call at 11:00 AM ET on Thursday, February 14, 2019 by dialing +1 (866) 843-0890 within the U.S., or +1 (412) 317-6597, and requesting the “Bluerock Residential Conference.”

For those who are not available to listen to the live call, the conference call will be available for replay on the Company’s website two hours after the call concludes, and will remain available until March 14, 2019 at http://services.choruscall.com/links/brg190214.html, as well as by dialing +1 (877) 344-7529 in the U.S., or +1 (412) 317-0088 internationally, and requesting conference number 10127798.

The full text of this Earnings Release and additional Supplemental Information is available in the Investor Relations section on the Company’s website at https://www.bluerockresidential.com.

About Bluerock Residential Growth REIT, Inc.

Bluerock Residential Growth REIT, Inc. (NYSE American: BRG) is a real estate investment trust that focuses on developing and acquiring a diversified portfolio of institutional-quality highly amenitized live/work/play apartment communities in demographically attractive knowledge economy growth markets to appeal to the renter by choice. The Company’s objective is to generate value through off-market/relationship-based transactions and, at the asset level, through value add improvements to properties and operations. The Company is included in the Russell 2000 and Russell 3000 Indexes. BRG has elected to be taxed as a real estate investment trust (REIT) for U.S. federal income tax purposes.

For more information, please visit the Company’s website at www.bluerockresidential.com.

Forward Looking Statements

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 and other federal securities laws. These forward-looking statements are based upon the Company’s present expectations, but these statements are not guaranteed to occur. Furthermore, the Company disclaims any obligation to publicly update or revise any forward-looking statement to reflect changes in underlying assumptions or factors, of new information, data or methods, future events or other changes. Investors should not place undue reliance upon forward-looking statements. For further discussion of the factors that could affect outcomes, please refer to the risk factors set forth in Item 1A of the Company’s Annual Report on Form 10-K filed by the Company with the U.S. Securities and Exchange Commission (“SEC”) on March 13, 2018, and subsequent filings by the Company with the SEC. We claim the safe harbor protection for forward looking statements contained in the Private Securities Litigation Reform Act of 1995.

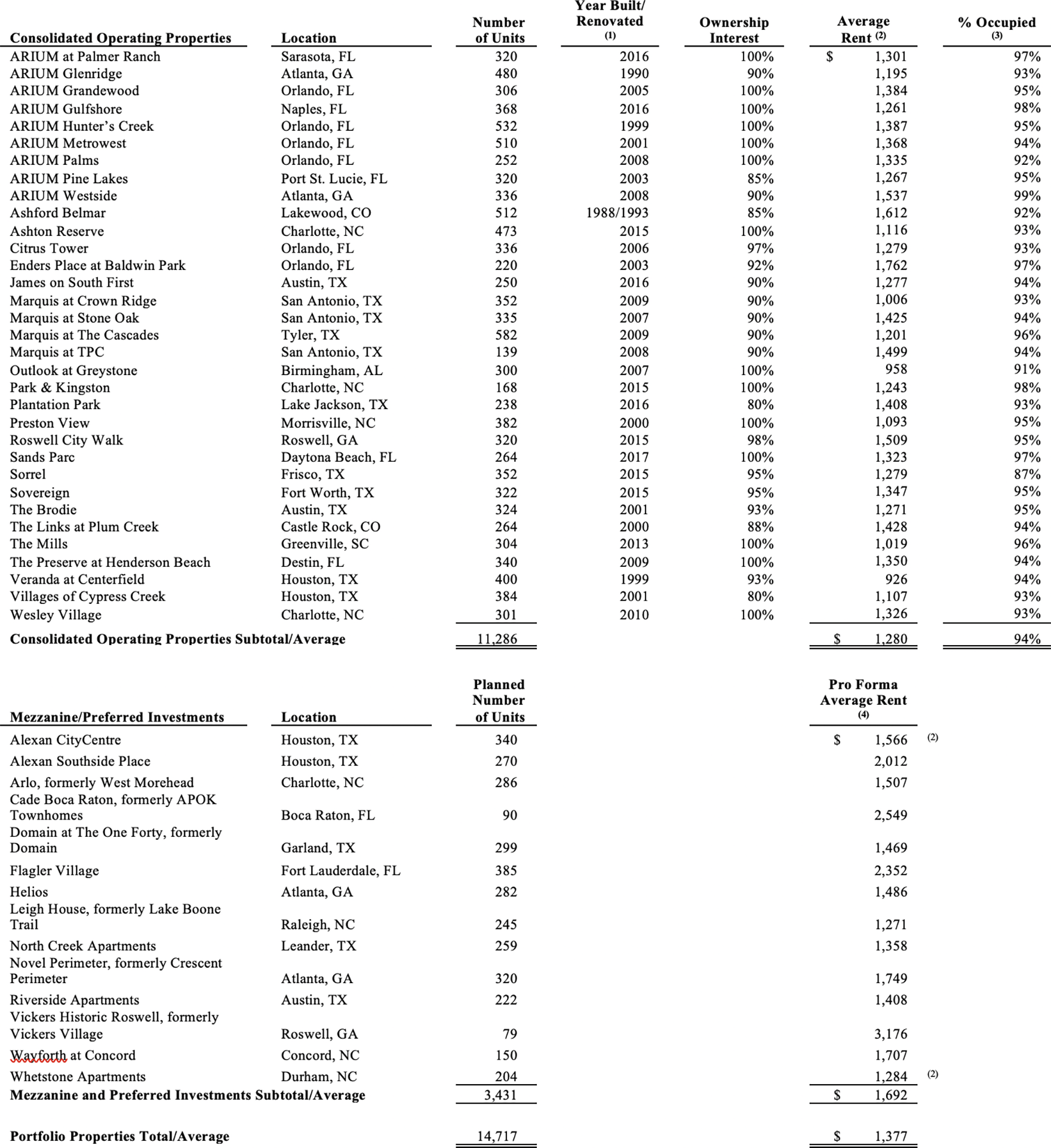

Portfolio Summary

The following is a summary of our operating real estate and mezzanine/preferred investments as of December 31, 2018:

(1) Represents date of last significant renovation or year built if there were no renovations.

(2) Represents the average effective monthly rent per occupied unit for the three months ended December 31, 2018.

(3) Percent occupied is calculated as (i) the number of units occupied as of December 31, 2018, divided by (ii) total number of units, expressed as a percentage.

(4) Alexan CityCentre, Alexan Southside Place, Helios, Leigh House, North Creek Apartments, Riverside Apartments, Wayforth at Concord, and Whetstone Apartments are preferred equity investments. Leigh House has the option to convert to indirect common interest in the property once the property reaches 70% occupancy. North Creek Apartments, Riverside Apartments, and Wayforth at Concord have the option to purchase the property at stabilization. Arlo, Cade Boca Raton, Domain at The One Forty, Flagler Village, Novel Perimeter, and Vickers Historic Roswell are mezzanine loan investments. Additionally, Arlo, Cade Boca Raton, Domain at The One Forty, and Vickers Historic Roswell have an option to purchase indirect property interest upon maturity.

Consolidated Statement of Operations

For the Three and Twelve Months Ended December 31, 2018 and 2017

(Unaudited and dollars in thousands except for share and per share data)

Consolidated Balance Sheets

Fourth Quarter 2018

(Unaudited and dollars in thousands except for share and per share amounts)

Non-GAAP Financial Measures

The foregoing supplemental financial data includes certain non-GAAP financial measures that we believe are helpful in understanding our business and performance, as further described below. Our definition and calculation of these non-GAAP financial measures may differ from those of other REITs, and may, therefore, not be comparable.

Funds from Operations, Core Funds from Operations, and Adjusted Funds from Operations

We believe that funds from operations (“FFO”), as defined by the National Association of Real Estate Investment Trusts (“NAREIT”), core funds from operations (“CFFO”), and adjusted funds from operations (“AFFO”) are important non-GAAP supplemental measures of operating performance for a REIT.

FFO attributable to common shares and units is a non-GAAP financial measure that is widely recognized as a measure of REIT operating performance. We consider FFO to be an appropriate supplemental measure of our operating performance as it is based on a net income analysis of property portfolio performance that excludes non-cash items such as depreciation. The historical accounting convention used for real estate assets requires straight-line depreciation of buildings and improvements, which implies that the value of real estate assets diminishes predictably over time. Since real estate values historically rise and fall with market conditions, presentations of operating results for a REIT, using historical accounting for depreciation, could be less informative. We define FFO, consistent with the NAREIT definition, as net income, computed in accordance with GAAP, excluding gains (or losses) from sales of property, plus depreciation and amortization of real estate assets, plus impairment write-downs of depreciable real estate, and after adjustments for unconsolidated partnerships and joint ventures. Adjustments for unconsolidated partnerships and joint ventures will be calculated to reflect FFO on the same basis.

CFFO makes certain adjustments to FFO, removing the effect of items that do not reflect ongoing property operations such as stock compensation expense, acquisition expenses, unrealized gains and losses on derivatives, losses on extinguishment of debt and debt modification costs (includes prepayment penalties incurred and the write-off of unamortized deferred financing costs and fair market value adjustments of assumed debt), non-cash interest, one-time weather-related costs, and preferred stock accretion. We believe that CFFO is helpful to investors as a supplemental performance measure because it excludes the effects of certain items which can create significant earnings volatility, but which do not directly relate to our core recurring property operations. As a result, we believe that CFFO can help facilitate comparisons of operating performance between periods and provides a more meaningful predictor of future earnings potential.

AFFO makes certain adjustments to CFFO in order to arrive at a more refined measure of the operating performance of our portfolio. There is no industry standard definition of AFFO and practice is divergent across the industry. AFFO adjusts CFFO for items that impact our ongoing operations, such as subtracting recurring capital expenditures (and while we were externally managed, when calculating the quarterly incentive fee paid to our former Manager only, we further adjusted FFO to include any realized gains or losses on our real estate investments). We believe that AFFO is helpful to investors as a meaningful supplemental indicator of our operational performance.

Our calculation of CFFO and AFFO differs from the methodology used for calculating CFFO and AFFO by certain other REITs and, accordingly, our CFFO and AFFO may not be comparable to CFFO and AFFO reported by other REITs. Our management utilizes FFO, CFFO, and AFFO as measures of our operating performance after adjustment for certain non-cash items, such as depreciation and amortization expenses, and acquisition and pursuit costs that are required by GAAP to be expensed but may not necessarily be indicative of current operating performance and that may not accurately compare our operating performance between periods. Furthermore, although FFO, CFFO, AFFO and other supplemental performance measures are defined in various ways throughout the REIT industry, we also believe that FFO, CFFO, and AFFO may provide us and our stockholders with an additional useful measure to compare our financial performance to certain other REITs. While we were externally managed, we also used AFFO for purposes of determining the quarterly incentive fee paid to our former Manager in prior periods.

Neither FFO, CFFO, nor AFFO is equivalent to net income, including net income attributable to common stockholders, or cash generated from operating activities determined in accordance with GAAP. Furthermore, FFO, CFFO, and AFFO do not represent amounts available for management’s discretionary use because of needed capital replacement or expansion, debt service obligations or other commitments or uncertainties. Neither FFO, CFFO, nor AFFO should be considered as an alternative to net income, including net income attributable to common stockholders, as an indicator of our operating performance or as an alternative to cash flow from operating activities as a measure of our liquidity.

We have acquired interests in five additional operating properties and three investments accounted for on the equity method of accounting subsequent to December 31, 2017. Therefore, the results presented in the table below are not directly comparable and should not be considered an indication of our future operating performance.

The table below reconciles our calculations of FFO, CFFO and AFFO to net loss, the most directly comparable GAAP financial measure, for the three and twelve months ended December 31, 2018 and 2017 (in thousands, except per share amounts):

(1) The real estate depreciation and amortization amount includes our share of consolidated real estate-related depreciation and amortization of intangibles, less amounts attributable to noncontrolling interests – partially owned properties, and our similar estimated share of unconsolidated depreciation and amortization, which is included in earnings of our unconsolidated real estate joint venture investments.

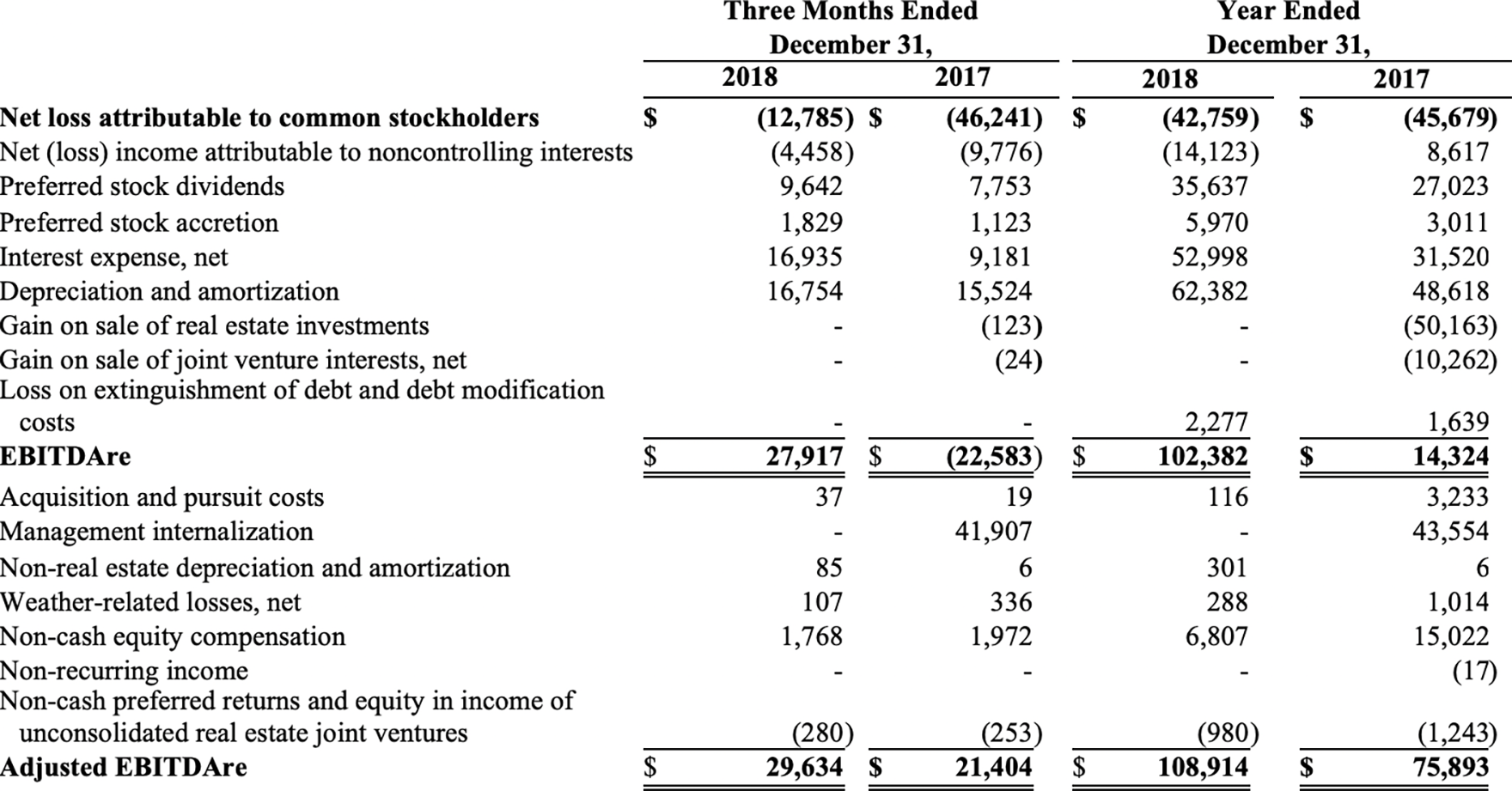

Earnings Before Interest, Taxes, Depreciation and Amortization for Real Estate (“EBITDAre”)

NAREIT defines earnings before interest, taxes, depreciation and amortization for real estate (“EBITDAre”) (September 2017 White Paper) as net income, computed in accordance with GAAP, before interest expense, income taxes, depreciation and amortization expense, and further adjusted for gains and losses from sales of depreciated operating properties, and impairment write-downs of depreciated operating properties.

We consider EBITDAre to be an appropriate supplemental measure of our performance because it eliminates depreciation, income taxes, interest and non-recurring items, which permits investors to view income from operations unobscured by non-cash items such as depreciation, amortization, the cost of debt or non-recurring items.

Adjusted EBITDAre represents EBITDAre further adjusted for non-comparable items and it is not intended to be a measure of free cash flow for our management’s discretionary use, as it does not consider certain cash requirements such as income tax payments, debt service requirements, capital expenditures and other fixed charges.

EBITDAre and Adjusted EBITDAre are not recognized measurements under GAAP. Because not all companies use identical calculations, our presentation of EBITDAre and Adjusted EBITDAre may not be comparable to similarly titled measures of other companies.

Below is a reconciliation of net loss attributable to common stockholders to EBITDAre (unaudited and dollars in thousands).

Recurring Capital Expenditures

We define recurring capital expenditures as expenditures that are incurred at every property and exclude development, investment, revenue enhancing and non-recurring capital expenditures.

Non-Recurring Capital Expenditures

We define non-recurring capital expenditures as expenditures for significant projects that upgrade units or common areas and projects that are revenue enhancing.

Same Store Properties

Same store properties are conventional multifamily residential apartments which were owned and operational for the entire periods presented, including each comparative period.

Property Net Operating Income (“Property NOI”)

We believe that net operating income, or NOI, is a useful measure of our operating performance. We define NOI as total property revenues less total property operating expenses, excluding depreciation and amortization and interest. Other REITs may use different methodologies for calculating NOI, and accordingly, our NOI may not be comparable to other REITs. We believe that this measure provides an operating perspective not immediately apparent from GAAP operating income or net income. We use NOI to evaluate our performance on a same store and non-same store basis; NOI measures the core operations of property performance by excluding corporate level expenses and other items not related to property operating performance and captures trends in rental housing and property operating expenses. However, NOI should only be used as a supplemental measure of our financial performance.

Certain amounts in prior periods, including related to tenant reimbursements for utility expenses amounting to zero and $3.0 million for the three and twelve months ended December 31, 2017, have been reclassified to other property revenues from property operating expenses, to conform to the current period. In addition, property management fees have been reclassified from property operating expenses.

The following table reflects net loss attributable to common stockholders together with a reconciliation to NOI and to same store and non-same store contributions to consolidated NOI, as computed in accordance with GAAP for the periods presented (unaudited and amounts in thousands):

(1) Same store portfolio for the three months ended December 31, 2018 consists of 24 properties, which represent 7,962 units. Same store portfolio for the year ended December 31, 2018 consists of 16 properties, which represent 5,151 units.